Key Highlights

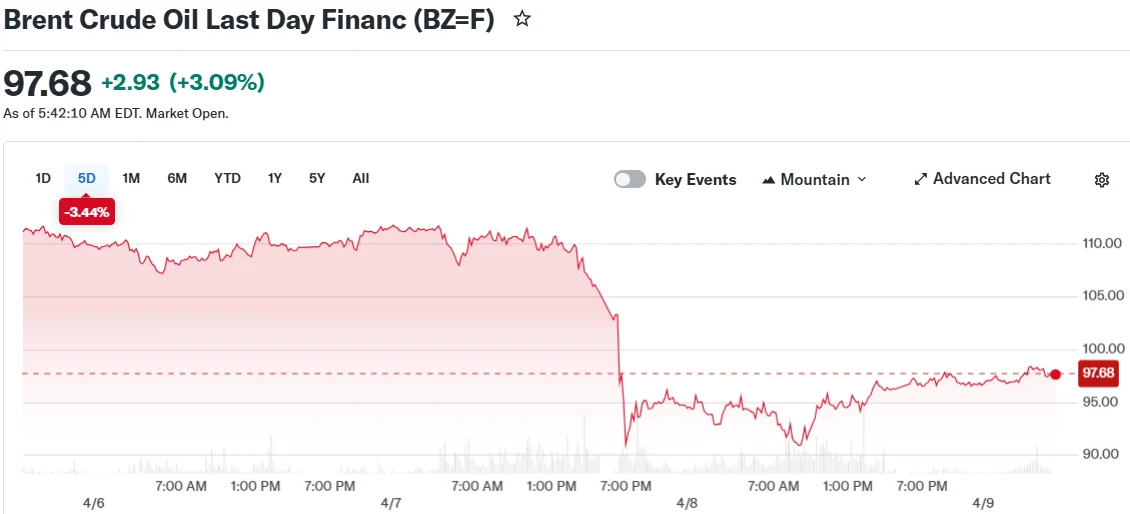

- Brent and WTI crude futures advanced approximately 3% Thursday following Wednesday’s 13%-plus collapse

- Wednesday’s selloff followed President Trump’s announcement of a temporary ceasefire agreement with Iran

- Ongoing Israeli military operations in Lebanon cast uncertainty on the ceasefire’s effectiveness

- Tehran continues blocking oil tanker passage through the Strait of Hormuz

- Goldman Sachs projects Brent averaging over $100 per barrel if the critical waterway remains shut for 30 more days

Crude oil markets staged a notable recovery Thursday after experiencing their steepest single-session decline since the pandemic began in April 2020. Brent futures advanced 2.8% to reach $97.68 per barrel, while West Texas Intermediate gained 3.3% to settle at $97.50 per barrel.

Wednesday’s dramatic market retreat followed President Donald Trump’s declaration of a two-week cessation of hostilities with Tehran. Market participants initially interpreted this development as indicating an imminent resolution to supply constraints.

However, optimism proved short-lived. Despite the ceasefire announcement, Israeli forces maintained offensive operations against targets throughout Lebanese territory, creating confusion about the agreement’s actual parameters.

Tel Aviv clarified that its military campaign against Hezbollah falls outside the ceasefire framework. Tehran responded by characterizing peace negotiations with Washington as “unreasonable” given present circumstances and alleging Israeli violations of the arrangement.

Tehran has maintained its suspension of oil tanker movements through the Strait of Hormuz. This critical maritime chokepoint facilitates approximately 25% of global seaborne petroleum commerce and has remained substantially closed following the February U.S.-Israeli military operation against Iran.

Goldman Sachs Projects Multiple Price Pathways

Goldman Sachs commodity strategists cautioned that prolonged closure of the strait through May could drive Brent prices to average beyond $100 per barrel during the latter half of 2026.

Their baseline projection anticipates shipping activity resuming this weekend, with Persian Gulf export volumes returning to pre-conflict levels within 30 days. This scenario places Brent at an $82 average for the third quarter and $80 for the fourth quarter.

A more pessimistic scenario incorporating extended closure duration and regional production losses would push Brent to $120 during Q3 and $115 in Q4.

Goldman’s research team indicated that forecast risks are “skewed to the upside.” Vice President JD Vance was separately quoted characterizing the ceasefire arrangement as tenuous.

Trump stated via social media that reopening the Strait of Hormuz to secure maritime traffic had been agreed upon “a long time ago.” He cautioned that military operations against Iran could recommence if agreement terms are not fulfilled.

American Crude Inventories Surge to Three-Year Peak

The U.S. Energy Information Administration disclosed that domestic crude reserves increased by 3.1 million barrels to reach 464.7 million barrels during the week concluded April 3. This represents the highest stockpile level observed in nearly 36 months and significantly exceeded analyst projections of a 1 million barrel build.

Refined product inventories presented contrasting trends. Distillate reserves, encompassing diesel fuel and heating oil, declined by 3.1 million barrels driven by robust export activity. Gasoline stockpiles decreased by 1.6 million barrels.

Iran’s Ports and Maritime Organization designated two authorized safe passage corridors for maritime vessels traversing the strait, both concentrated around Larak Island in proximity to Bandar Abbas.

ING commodity analysts suggested that complete restoration of strait operations remains improbable in the immediate term, with prices likely to maintain support as supply disruptions require considerable time to normalize.

Brent futures had previously reached $119.50 during the conflict’s peak intensity before plummeting Wednesday on ceasefire developments.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants