Stock Surges 5% Ahead of Historic Nasdaq Debut")

TLDR

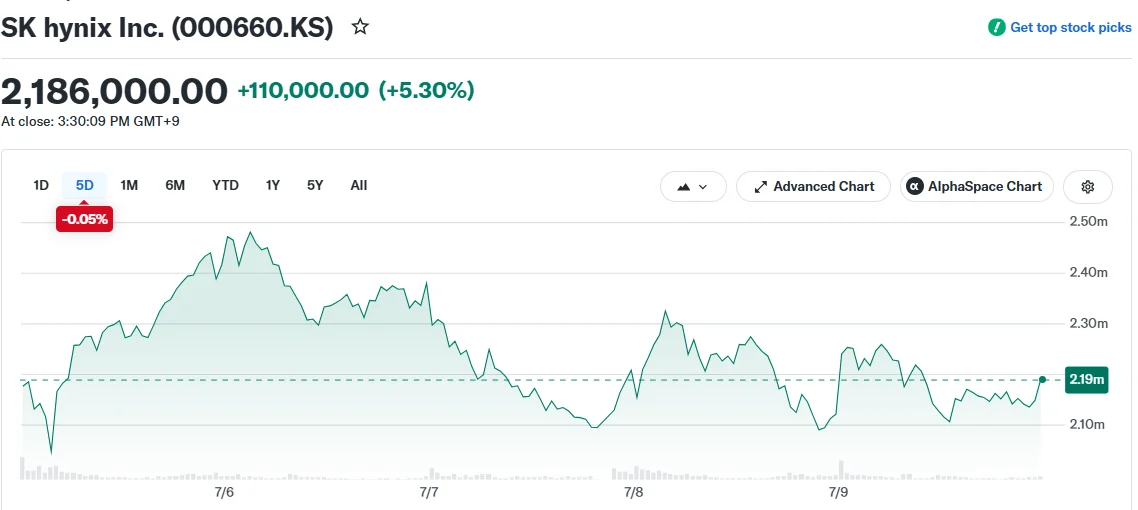

- SK Hynix shares climbed 5.3% in Seoul trading Thursday before its Friday Nasdaq ADR debut under ticker SKHY

- The American depositary receipt offering attracted seven times more demand than shares available, with 177.9 million ADRs on offer

- Based on Thursday’s closing price, the deal could generate $25.71 billion—potentially the biggest ADR offering ever recorded

- Each ADR package consists of one-tenth of a Korean share, suggesting an approximate price of $144.50 per ADR

- Institutional heavyweights, including the Situational Awareness hedge fund, have committed to purchasing as much as $7 billion in the offering

Shares of SK Hynix surged 5.3% during Seoul trading hours on Thursday, finishing at 2.186 million won (approximately $1,445), as market participants braced for the semiconductor giant’s much-awaited Nasdaq ADR launch.

Scheduled to begin trading Friday under the SKHY ticker symbol, the offering has already attracted extraordinary interest from institutional buyers. Reports from Bloomberg indicate the subscription closed Wednesday with demand reaching seven times the available supply.

A consortium of investment banks led by Goldman Sachs, Citi, Bank of America, and JPMorgan is managing the placement of 177.9 million newly issued ADRs. Final pricing details are anticipated Thursday evening, with allocation notifications to follow shortly after.

Each American depositary receipt represents one-tenth of a Korean-listed share, translating to an estimated ADR price near $144.50. While some portfolio managers anticipated a modest discount to entice buyers, at least one London-based fund manager indicated the robust institutional appetite might eliminate any pricing discount entirely.

Using the projected pricing, SK Hynix stands to collect roughly $25.71 billion in proceeds, positioning this transaction to eclipse the previous ADR record holder—Alibaba’s $25 billion American listing completed in 2014.

This offering would also secure the position as the second-largest equity capital raise in history, exceeded only by SpaceX. Remarkably, it would also edge out Saudi Aramco’s landmark 2019 initial public offering, which brought in $25.6 billion.

The final tally remains below SK Hynix’s original $29 billion objective, set before the Korean equity market entered technical correction territory in recent trading sessions.

Robust Interest Persists Despite Market Turbulence

Even with recent choppiness on the Korean Stock Exchange and a sharp correction in the company’s share price, investor enthusiasm has held firm. Situational Awareness, a hedge fund founded by a former OpenAI researcher, has publicly stated its intention to acquire up to $7 billion of the ADRs.

Emerging market specialists operating in London have observed that some of the recent softness in the Kospi benchmark may stem from fund managers liquidating positions to raise capital for the subscription. Additionally, the slight strengthening of the Korean won in recent sessions is being linked to SK Hynix establishing hedges for the anticipated dollar inflows it expects to convert back to local currency.

Valuation Appears Reasonable Despite Massive Rally

Notwithstanding a remarkable 235% year-to-date gain in South Korean trading and a staggering 600% advance over the trailing twelve months, SK Hynix maintains surprisingly attractive valuation metrics.

Based on FactSet consensus figures, the company currently trades at merely 5.5 times projected earnings. Equity analysts have repeatedly raised their profit forecasts as insatiable demand for the company’s DRAM and NAND memory products continues to exceed manufacturing capacity.

The Nasdaq listing provides American investors with direct access to the memory chip sector’s explosive growth. Previously, Micron Technology (MU) served as the primary vehicle for U.S. investors seeking this exposure—shares of Micron were already trading 3.4% higher in premarket activity Thursday.

As South Korea’s second-largest publicly traded company, SK Hynix faces a situation similar to Samsung Electronics: its production pipeline cannot satisfy current customer demand. This fundamental supply-demand mismatch has consistently driven upward pressure on the average selling prices of its semiconductor products.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants