TLDR

- Equity futures advanced Monday morning, with Dow futures gaining 0.4% and S&P 500 futures rising 0.2% before the opening bell

- May saw the Nasdaq jump more than 8%, marking its strongest consecutive two-month performance since 2002 when paired with April’s 25% surge

- Technology and artificial intelligence sector earnings propelled the historic rally throughout May

- Middle East conflict between Washington and Tehran continues following weekend military actions, supporting elevated crude prices

- This week’s nonfarm payrolls data on Friday represents the primary catalyst market participants are monitoring

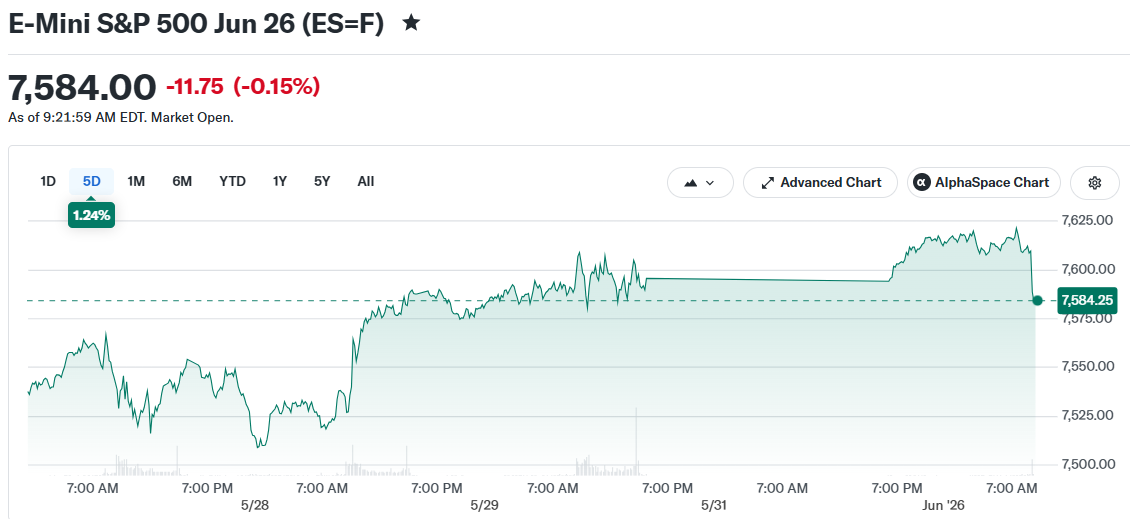

Equity futures advanced Monday morning as market participants sought to carry forward the impressive momentum from May into the new trading month.

Futures tied to the Dow Jones Industrial Average rose 0.4%, with S&P 500 futures climbing 0.2%. Futures linked to the Nasdaq 100 similarly advanced 0.2% during early session activity.

The morning advances build upon a robust conclusion to May trading. The Nasdaq Composite posted gains exceeding 8% during the previous month, and together with April’s 25% climb, represents the strongest consecutive two-month stretch for the technology-heavy benchmark since the final months of 2002.

The S&P 500 advanced approximately 5% throughout May. The Dow Jones Industrial Average registered gains approaching 3% during the identical timeframe.

Each of the three primary benchmarks concluded last week at unprecedented peak levels. Technology equities have primarily fueled the advance, with AI chipmakers capturing substantial capital from market participants.

Robust quarterly results from technology corporations have served as a primary catalyst. Financial markets have handsomely compensated numerous leading companies operating within the artificial intelligence and semiconductor industries.

Middle East Tensions Add Market Complexity

Notwithstanding the optimistic market sentiment, geopolitical developments continue presenting challenges. American military aircraft targeted Iranian radar installations and unmanned aerial vehicle facilities during the weekend, with Iran’s Islamic Revolutionary Guard Corps announcing retaliatory measures.

President Trump indicated he would consult with senior advisers to reach a “final determination” regarding future actions. He additionally demanded the immediate restoration of commercial traffic through the Strait of Hormuz, a critical waterway for international energy transportation.

Oil prices strengthened following the weekend military operations. Brent crude advanced 3.1% reaching $93.98 per barrel, while West Texas Intermediate gained 3% trading at $90.40 per barrel.

Despite Monday’s recovery, WTI registered its most significant monthly decline since April 2025, dropping nearly 17% throughout May.

The greenback strengthened 0.1% versus a collection of major global currencies. The benchmark 10-year Treasury note yield increased 2 basis points to 4.47%, reflecting investor movement toward defensive positions.

Deutsche Bank analyst Jim Reid said the outlook for June will depend heavily on whether a US-Iran deal materializes. “We’ve never felt closer to a deal but potentially never felt closer to it all falling apart,” he said.

Employment Data Takes Center Stage

Market participants will closely examine Friday’s nonfarm payrolls release. The employment statistics will provide updated insights regarding labor market conditions and may shape predictions for Federal Reserve monetary policy adjustments throughout the remainder of the year.

Expectations surrounding a potential diplomatic agreement between Washington and Tehran had supported market sentiment during recent trading sessions. Nevertheless, the weekend military strikes have generated renewed uncertainty regarding the timeline for any potential resolution.

Financial markets continue operating in a cautious posture concerning geopolitical developments, with investors weighing robust technology sector performance against persistent Middle East instability.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants