Key Takeaways

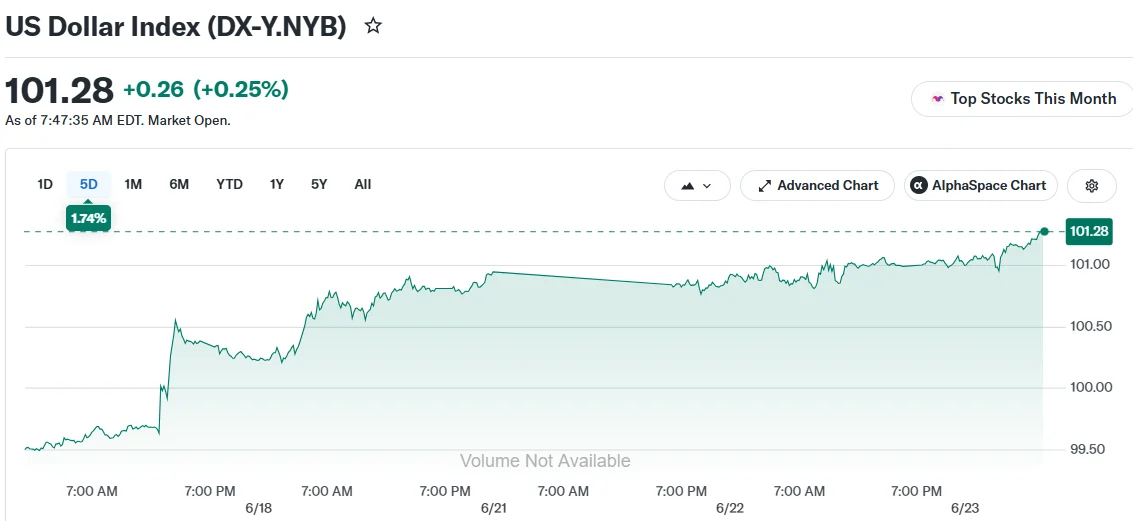

- The US Dollar Index surged to 101.25, marking its strongest level in more than 12 months

- Market expectations now show an 80–85% probability of a Federal Reserve rate increase by fall

- Japan’s yen hovers dangerously close to its weakest position since 1986, sparking intervention concerns

- Political upheaval in the UK following Prime Minister Keir Starmer’s resignation weighs on the pound

- The euro dropped to its lowest point since August 2025 following dovish remarks from ECB President Lagarde

Currency markets witnessed significant volatility on Tuesday as the US dollar surged to its highest point in over a year, driven by escalating expectations that the Federal Reserve will tighten monetary policy before year-end. The Dollar Index reached 101.25, a level not seen since May 2025.

Market indicators now reflect approximately 80 to 85% odds of a 25-basis-point interest rate increase by late summer or early autumn. Major financial institutions including BofA Global Research and Deutsche Bank have adjusted their projections, abandoning previous predictions of unchanged policy in favor of anticipating a rate adjustment within 2025.

“Right now, the dollar is pricing in higher rates and is gaining on that,” said Tommy von Bromsen, FX strategist at Handelsbanken.

The greenback is receiving additional support from persistent geopolitical risks stemming from unresolved conflicts in the Middle East, von Bromsen noted.

Japanese Yen Teeters on Brink of Four-Decade Milestone

Japan’s currency finds itself in precarious territory. The yen momentarily touched 161.93 against the dollar during Monday’s trading session, with a breach above 161.96 threatening to send it to depths not witnessed since 1986.

Financial markets remain vigilant for possible intervention from Japanese monetary authorities. Tokyo deployed substantial resources—tens of billions of dollars—during late April and early May attempting to support the currency, though these measures yielded only temporary relief.

The Bank of Japan implemented an interest rate increase last week and communicated intentions for additional policy tightening moving forward. Despite these actions, the yen has continued its descent, undermined by the substantial differential between American and Japanese borrowing costs.

Japanese Finance Minister Satsuki Katayama engaged in discussions with US Treasury Secretary Scott Bessent on Monday. The consultation centered on coordinated policy measures addressing the yen’s depreciation, including potential foreign exchange market intervention.

UK Political Drama Pressures Sterling, Euro Weakens on ECB Tone

The British pound declined between 0.2 and 0.3% on Tuesday following UK Prime Minister Keir Starmer‘s resignation announcement, injecting fresh political instability into British financial markets. Health Minister Wes Streeting’s endorsement of Andy Burnham as a successor helped calm some concerns about the leadership transition, according to market observers.

“With Streeting’s willingness to back Burnham, this uncertainty is now likely to be a thing of the past,” said Commerzbank FX analyst Michael Pfister.

The euro experienced its own decline, sliding to $1.1395—its weakest reading since August 2025. ECB President Christine Lagarde minimized concerns about secondary inflation effects during Monday remarks, while fresh data revealed eurozone private sector contraction for a third consecutive month in June.

The Australian dollar experienced a sharper decline of 0.7 to 0.8%, touching its lowest valuation since April.

Traders are now focusing attention on forthcoming US economic releases. Wednesday’s May PCE price index report—the Federal Reserve’s preferred inflation metric—heads a busy data calendar. June purchasing managers’ index figures and a revised first-quarter GDP estimate are also scheduled this week. These data points will likely dictate whether the dollar’s momentum can sustain itself in coming sessions.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants